Johannesburg, 25 June 2026: In South Africa, gambling is often spoken about as harmless background noise - a Lotto ticket bought in passing, a quick weekend bet, a small indulgence in a difficult economy. But that framing is becoming harder to defend according to the 2026 Sanlam Benchmark Survey which found 50% of respondents in the online consumer portion of the study had spent money on gambling, betting or lottery activities in the last three months. With 66% using salary and wages as the source of funds.

Nzwa Shoniwa, Managing Executive: Sanlam Umbrella Solutions, says this suggests that for many people, gambling is no longer simply about entertainment. “It is increasingly bound up with financial pressure, short-term coping and the trade-off between immediate relief and long-term security.”

The 2026 Sanlam Benchmark - the country’s most comprehensive retirement fund industry research - surveyed 76 standalone funds, 130 umbrella fund employers, 30 pensioners who retired four to five years ago, and 600 consumers who are nearing or in retirement.

Shoniwa says the Benchmark found participation to be notably higher among those still economically active, especially for the more frequent, more digital and potentially riskier forms of gambling. “Retirees are not untouched, but the intensity is lower. The bigger risk is the pre-retirement habit that chips away at financial resilience over time.”

Entertainment on the surface, financial pressure underneath

The majority of respondents, 58%, still describe gambling as entertainment. But that headline number does not tell the full story. The survey shows that 38% gamble to generate additional income, while others cite stress relief or trying to recover losses. That shifts the picture considerably.

Among working South Africans, gambling is more closely tied to cash-flow pressure. Among retirees, it is more often seen as a possible income top-up. In both cases, gambling starts to move away from recreation and closer to coping.

The digital shift matters

Lotto and scratch cards still dominate, with roughly 72% of those who gamble saying they spend money there. But the bigger shift is happening elsewhere. Online sports betting and casino gambling now account for more than a third of activity each. That matters because these formats make repeated spending easier, quicker and less visible. Retirees tend to stay closer to Lotto-style play. Working South Africans are more likely to be in the higher-frequency online space, where small, regular spending can quietly crowd out saving over time.

The frequency data reinforces the point. The most common pattern is gambling a few times a month (33%), with weekly or near-weekly participation also significant among people who are not yet retired. In a low-savings environment, modest but repeated spending can do real damage over time.

This frequency dynamic is critical. As the report notes, the real financial risk lies in “small regular leaks”, modest but consistent spending that gradually crowds out savings. In an environment where many households already face budget pressure, repeated discretionary spend, even at low levels, can accumulate into meaningful long-term financial erosion.

Gambling is not being funded with spare cash

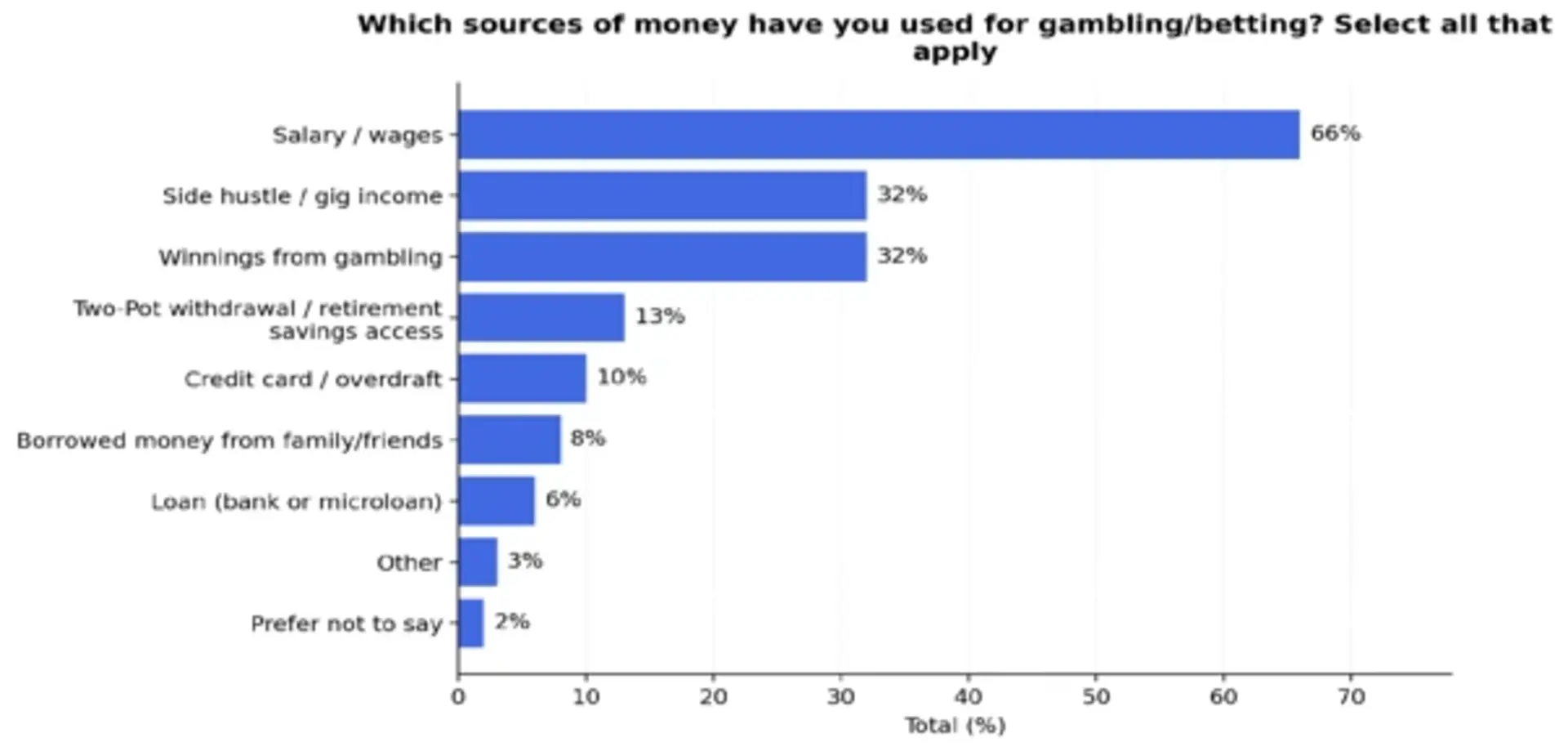

Perhaps the most sobering finding is where the money comes from. In many cases, gambling is not funded from “extra” income. It comes straight out of salary or wages, which 66% of respondents say they use to gamble, with some also drawing on side-hustle income, credit, borrowed money and even two-pot retirement withdrawals. That should immediately reframe the conversation: this is not only leisure spend, but money that might otherwise support financial resilience.

Financial stress is the backdrop

These behaviours do not happen in isolation. They sit inside a much wider story of financial strain. In last year’s Benchmark survey, more than 80% of respondents said they were experiencing financial stress. That pressure does not only affect household budgets. It also affects mental health, decision-making and workplace wellbeing.

That is why this should matter beyond the gambling conversation. Persistent financial anxiety creates conditions in which short-term choices can override long-term interests. It also helps explain why employers are seeing rising absenteeism linked to stress, anxiety and mental-health strain in the benchmark findings over the past two years.

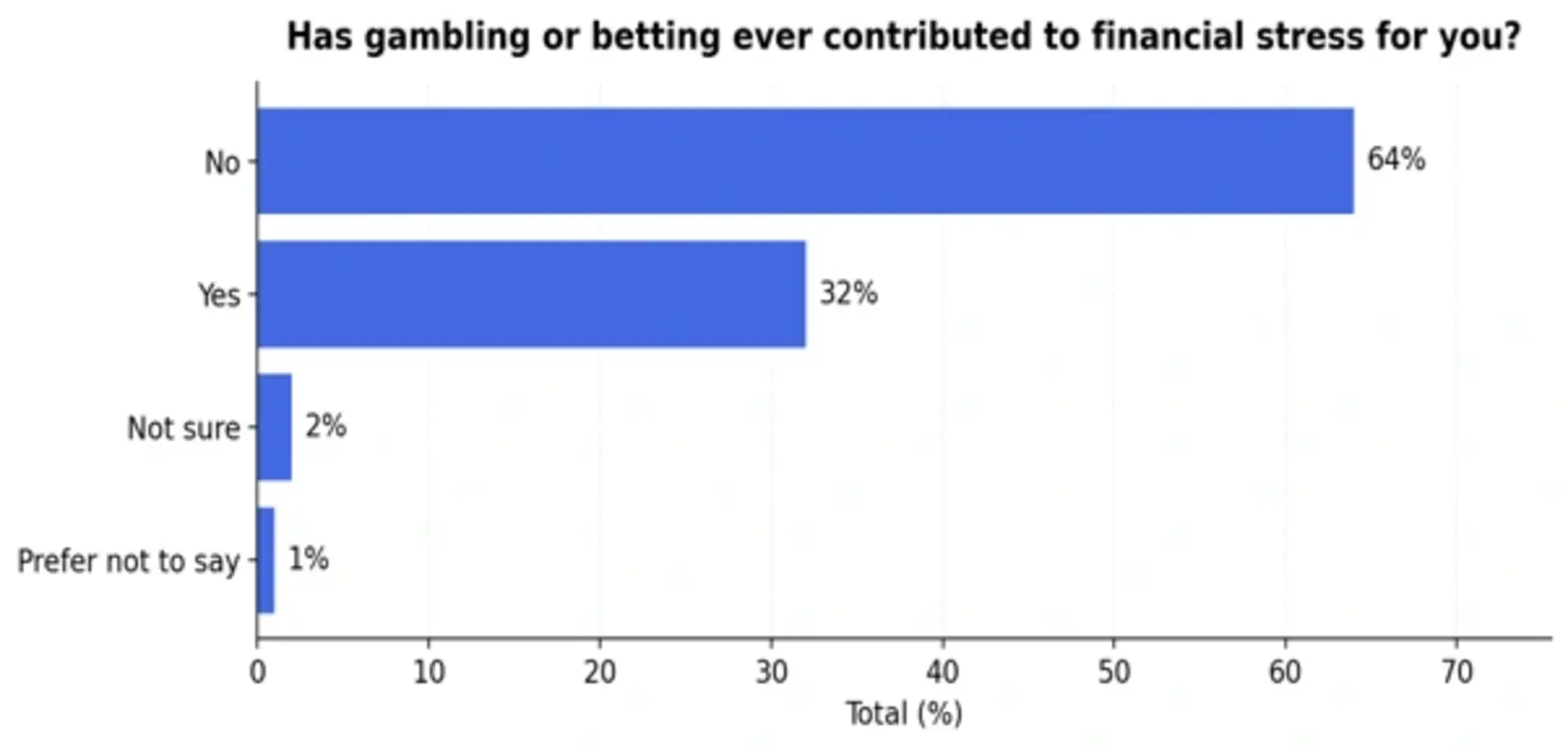

A full 32% of respondents say gambling has contributed to financial stress. That is a sizeable minority, and in some cases an early warning sign of deeper financial vulnerability.

32% of respondents say gambling has contributed to financial stress.

Not just a gambling story: Financial strain becoming a workplace issue

Shoniwa believes the findings should prompt a broader rethink by employers, funds, advisers and policymakers. “The bigger issue here is not morality, but financial behaviour under pressure.”

The Sanlam Benchmark 2026 findings suggest that gambling is becoming one of the ways financial strain shows up in everyday life, with implications not only for savings and retirement readiness, but also for mental health, workplace performance and household stability. That makes this a stronger case for holistic employee wellbeing solutions, especially those that bring together financial education, mental health support and accessible employee assistance programmes.

He says investing in employee wellbeing should not be seen as a soft benefit or a peripheral HR intervention. In a low-savings, high-stress environment, it is part of protecting the health of the workforce and, by extension, the resilience of the economy.

“When employees have access to support that helps them manage stress, debt, anxiety and difficult financial choices earlier, employers are not only investing in the people who work for them. They are contributing to a more financially stable, mentally healthier and ultimately more productive society. That is the broader lesson in the data: financial vulnerability does not stay confined to the individual. It carries consequences that ripple outward into workplaces, families and the country’s long-term wellbeing,” Shoniwa says.

Ends