Debt consolidation seems more possible given the commodities bonanza

The National Treasury’s intent to return fiscal policy to sustainability is not in doubt but its track record in stabilizing the government debt ratio has been poor for years. This reflects the impact of the COVID-19 pandemic, spending associated with South Africa’s high unemployment rate (a consequence of low GDP growth) and bailouts of state-owned enterprises.

However, given improvements in tax administration, tapping into the Gold and Foreign Exchange Contingency Reserve Account on the Reserve Bank’s balance sheet and the timely bounce in export commodity prices, it seems reasonable to argue that fiscal year 2025/26 should signal the peak in the debt ratio, with decreases likely to be projected over the medium term commencing in 2026/27. After all, the boost to income from commodities may increase government revenue by around a three-quarter percent of GDP cumulatively.

That said, the entire revenue proceeds of the commodity bonanza are unlikely to be “saved” considering the needs generated by South Africa’s depression-level unemployment rate and dire socio-economic condition. Hence, the debt ratio is expected to remain high over the medium term with decreases in the ratio limited.

It would be helpful if the Treasury limited income tax increases

A popular assumption is that the National Treasury will use this good fortune to scale back its plans for new revenue-raising measures. In 2023/24 the tax-to-GDP ratio was 24.5%. Last year’s Medium Term Budget Policy Statement projected an increase in the ratio to 25.7% in 2025/26 and further to 26.4% in 2028/29, implying tax buoyancy above one over the medium term.

Households’ tax on income and wealth

It would be favourable if the Treasury focused on limiting income tax increases. Indeed, given South Africa’s relatively low VAT rate, I believe that a VAT increase in 2025/26 (albeit smaller than proposed) with appropriate additional zero-rating to protect the poor was preferable relative to the alternative chosen.

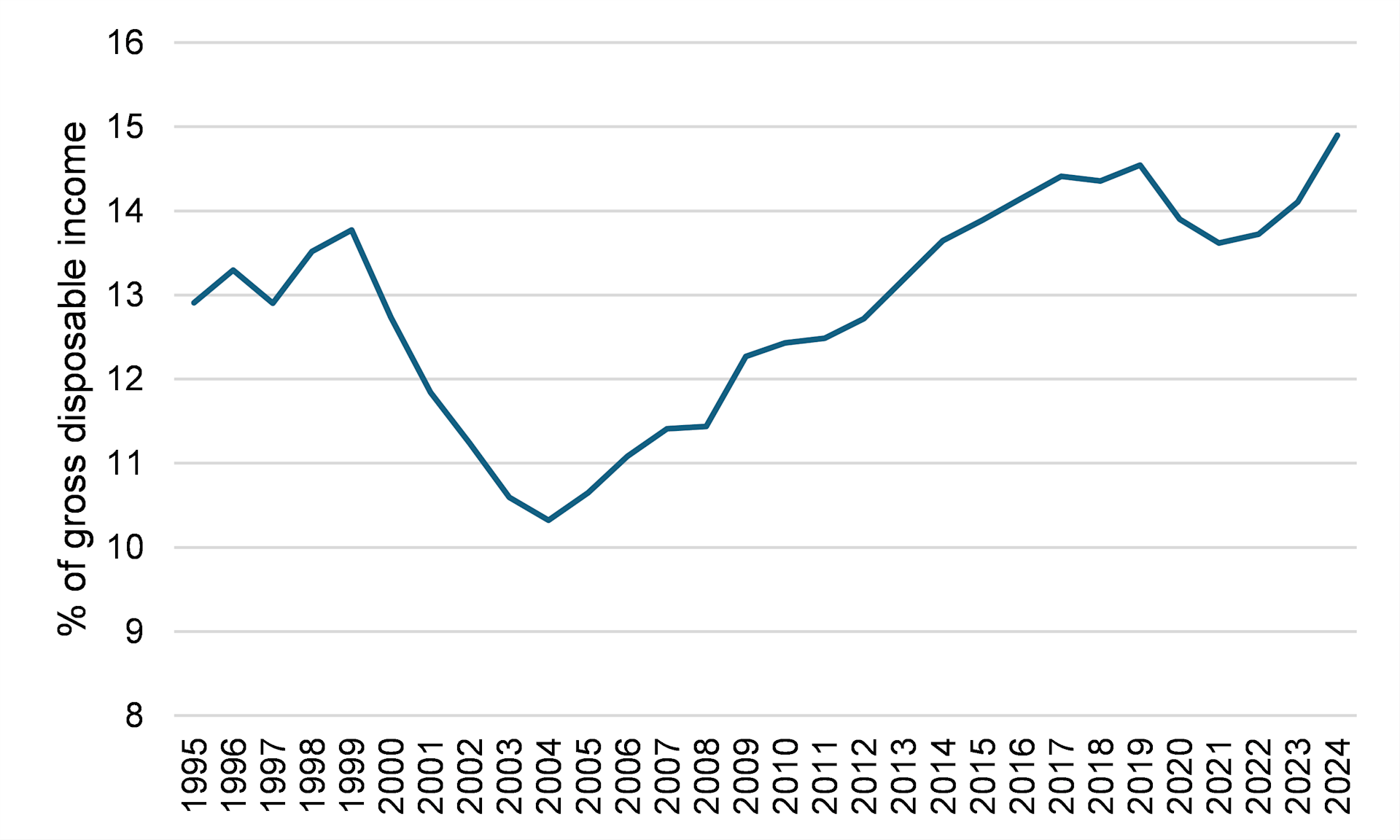

In the last two fiscal years, the Treasury has not adjusted income tax brackets or medical tax credits for inflation, implying an increase in the average tax rate for individuals. In its May 2025 Budget Overview, the Treasury estimated this would cost taxpayers R16.7 billion in 2025/26. Note there is also a carry-through effect in subsequent tax years. At the same time, it is worth noting the latest available annual data from the South African Reserve Bank shows individuals’ tax on income and wealth increased from 10.3% of gross disposable income in 2004 to 14.9% of gross disposable income in 2024.

The Treasury itself noted in its original (now defunct) 2025 Budget Review that increasing personal income tax is likely to be counter-productive since taxpayers typically find ways to reduce their tax liabilities in response. Or one could also argue higher income taxes reduce the incentive to work, save and invest.

The Treasury indicated last year it would seek an additional R20 billion in revenue raising measures in 2026/27. The expected increase in revenue due to the commodities bounce should obviate the need for this. Hopefully there is relief from bracket creep in Budget 2026.

This does not mean that tax increases are entirely off the table. For one thing, we do not know the extent to which the Treasury will adjust its projections for commodity prices and subsequently revenue collection. For example, in the 2025 MTBPS, the Treasury projected average gold and platinum prices of R3 968 per ounce and R1 520 per ounce respectively – well below levels at the time of writing.

Apart from the usual likely sin tax increases and potential upward adjustment to the fuel levy, other taxes being considered are an online gambling tax, although it is unlikely to be introduced in Budget 2026.

Better debt dynamics

Something to bear in mind is the impact of South Africa’s new inflation target. A large portion of government debt is long-term fixed interest debt. Lower expected inflation implies the real interest rate on this debt has increased.

Concomitantly, though, there are developments which should help stabilise and reduce the debt ratio. First, following the decrease in interest rates, which accompanied the adoption of a lower inflation target, government debt is no longer being issued at a large discount. Further, the appreciation of the rand and lower inflation have a favourable impact on the revaluation of foreign currency and inflation-linked bonds.

Meanwhile, the commodities boost to revenue should improve the primary budget surplus relative to current projections.

In addition, the bounce in commodity prices increases the GDP deflator. Together, these developments imply a slower pace of debt accumulation relative to GDP.

Lingering risks amid many moving parts

Things are looking better. That said there are many moving parts and risks, including potentially volatile global economic activity and commodity prices, which could influence fiscal outcomes in the years ahead.

As regards expenditure, the Treasury is appealing a court ruling which could substantially increase spending on social grants if the original decision is ultimately upheld. Also, spending on National Health Insurance remains a material upside long-term spending risk. Moreover, the current budget assumes the large-scale support for state owned enterprises, so evident for years, fades with the Treasury’s preference switching to the provision of guarantees with provisions. In the end, it may be difficult to hold the line on expenditure.

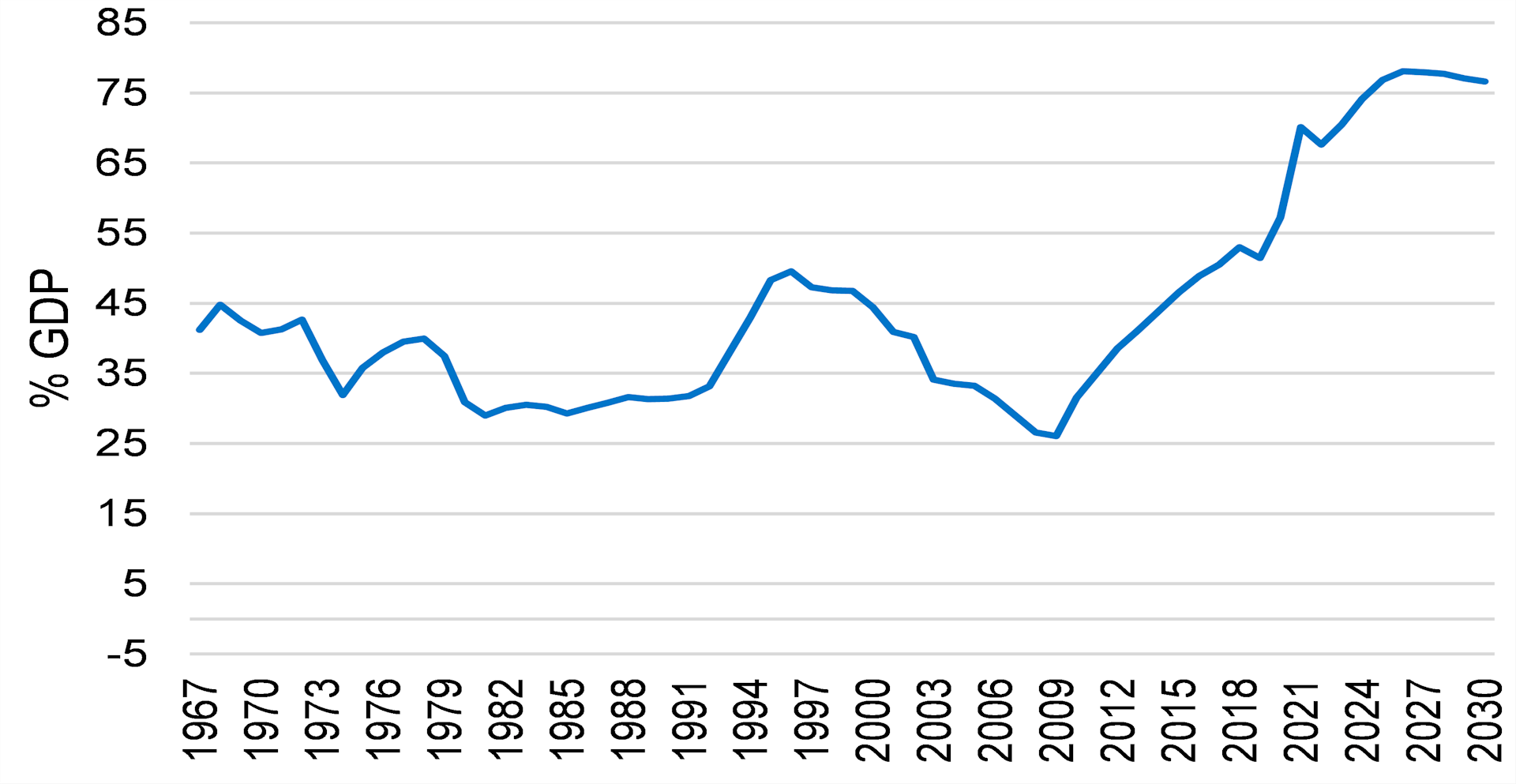

Gross loan debt ratio – actual and projected

Sustained primary budget surpluses are rare

Viewed more simplistically, it is no easy task to run a primary budget surplus for a sustained period against the backdrop of ailing service delivery. Indeed, through South Africa’s history, primary budget surpluses have been the exception rather than the rule. There is much discussion around an anticipated introduction of a fiscal rule for South Africa. This includes numerical fiscal rules which limit the debt level or fiscal deficits. However, this lacks flexibility and would require “escape clauses” for events such as the COVID-19 pandemic. Alternatively, the Treasury is considering a parliamentary procedures model, which embeds fiscal sustainability principles into the process of tabling and voting of budgets. If implemented, a fiscal rule would demonstrate commitment to fiscal consolidation.

In the end it’s about GDP growth

On balance, the above highlights the importance of growing the economy faster on a sustainable basis. Absent this, the fiscal math does not add up. In turn, this speaks to the need for the completion of South Africa’s economic reform programme. A good start has been made on improving electricity and transport infrastructure under Phase I of Operation Vulindlela. Attention now turns to Phase II, which includes a focus on structural reforms in local government.

Disclaimer: Sanlam Investments consists of authorised financial services providers in terms of FAIS and disclaimers can be viewed on https://www.sanlaminvestments.com/legal/disclaimer