The 2026 National Budget Speech, delivered by the Minister of Finance, Minister Enoch Godongwana on 25 February 2026, highlights South Africa’s progress toward fiscal stability and renewed economic confidence as the country moves beyond years of financial strain and structural challenges.

The update reflects a policy stance aimed at strengthening the resilience and credibility of South Africa’s financial system, supporting economic growth and inclusion, and positioning the country as a competitive financial hub, while maintaining robust safeguards against financial crime and systemic risk. It focuses on improving financial integrity following South Africa’s exit from the FATF grey list, modernising the regulatory environment, promoting fair consumer outcomes, enabling innovation in payments and digital finance, and implementing measures to strengthen competition, market conduct, climate risk readiness, and the management of unclaimed assets.

The 2026 Budget introduces inflationary adjustments to personal income tax brackets, tax thresholds, and rebates after two consecutive years of freezes. An enhancement to the tax-free savings investment by increasing the annual contribution limit from R 36 000 to R 46 000, and the annual deductible limit for retirement fund contributions has been increased from R 350 000 to R 430 000 per annum. No change to the percentage-based deduction (up to 27.5% of taxable income including fringe benefits) has been made.

Together, these policy measures reflect government’s commitment to building a more stable, inclusive and future ready financial system that supports sustainable growth and protects consumers.

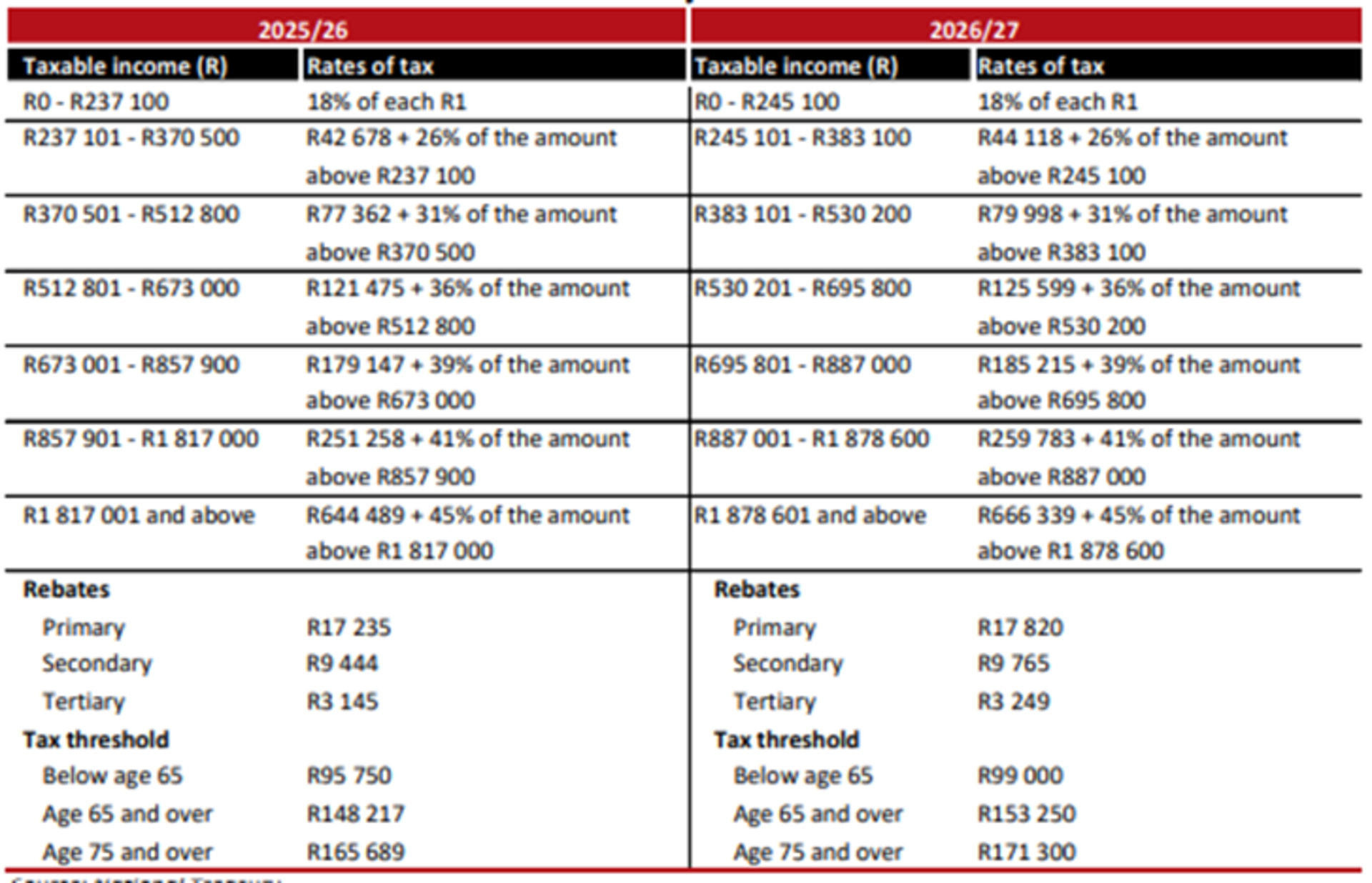

2.1 Personal income tax - individuals

After two years with no inflationary relief, personal income tax brackets and medical tax credits will be fully adjusted for inflation. Table 4.4 shows the amended tax brackets, thresholds and rebates for individual taxpayers:

2.2 Medical tax credits Medical tax credits will increase from R364 to R376 for the first two members, and from R246 to R254 for additional members.

2.3 Allowing rollover treatment of capital allowances on allowance assets transferred between spouses The Income Tax Act regulates the transfer of assets between spouses through section 9HB of the Act. This provision establishes a rollover mechanism for the transfer of trading stock, livestock and capital assets between spouses. However, the recoupment component of the rollover for allowance assets is not provided for, as section 9HB does not prevent the recoupment of capital allowances in the hands of the transferor spouse under section 8(4)(k) of the act, nor does it allow the transferee spouse to take over the accumulated allowances previously claimed. It is proposed that section 9HB be amended to prevent the recoupment of capital allowances on the transfer of allowance assets between spouses and to provide for the carry-over of accumulated allowances to the transferee spouse.

2.4 Limiting the donations tax exemption rules where a spouse ceases to be a tax resident Section 56 of the Income Tax Act exempts donations between spouses from donations tax. Government has become aware of tax avoidance arrangements, particularly involving high-net-worth individuals planning to cease to be South African tax residents. The arrangement involves deliberately staggering the cessation of tax residence between spouses where significant assets are transferred to a spouse who has already become non-resident before the remaining spouse ceases residence. In these circumstances, the donations tax exemption applies, while the subsequent cessation of tax residence by the remaining spouse results in a reduced income tax liability under section 9H of the Act. These arrangements are designed to avoid both donations tax and the income tax on cessation of residency, undermining the original policy intent of these provisions. It is proposed that the donations tax exemption rules applicable to spouses be limited to donations made to a spouse who is a resident effective from 25 February 2026.

2.5 Extending the eligibility for the medical scheme fees tax credit Certain statutory medical schemes face regulatory constraints that remove them from the authority of the Council for Medical Schemes. Consequently, individual members of these schemes are not eligible for the medical scheme fees tax credit under section 6A of the Income Tax Act. It is proposed that eligibility for this tax credit be extended to such members, provided that the schemes offer benefits, and adhere to governance and solvency requirements that are at least equivalent to those prescribed under the Medical Schemes Act (1998).

2.6 Increase in annual contribution limit to tax-free investments Currently, contributions to a tax-free investment are limited to R36 000 per annum, which annual limit has been in place since 2021. The annual limit will be increased to R46 000.

2.7 Single discretionary allowance To take account of inflation and currency fluctuations, the single discretionary allowance limit for private individuals is increased from R1 million to R2 million per calendar year via Authorised Dealers for all purposes, including travel, gifts, remittances, investments and donations. Permitted single discretionary allowance transfers via Authorised Dealers in foreign exchange with limited authority are increased from R1 million to R2 million. The limit will be reviewed regularly.

2.8 Increases to certain taxes The excise duties on tobacco will be increased in line with inflation. This includes excise duty on electronic nicotine and non-nicotine delivery systems. The excise on alcoholic beverages also rises by inflation.

In terms of fuel levies, the total increase will also be in line with inflation, and the general fuel levy will go up by 9 cents per litre for petrol and 8 cents per litre for diesel. The carbon fuel levy will go up by 5 cents per litre for petrol and 6 cents for diesel. The Road Accident Fund levy will increase by 7 cents per litre.

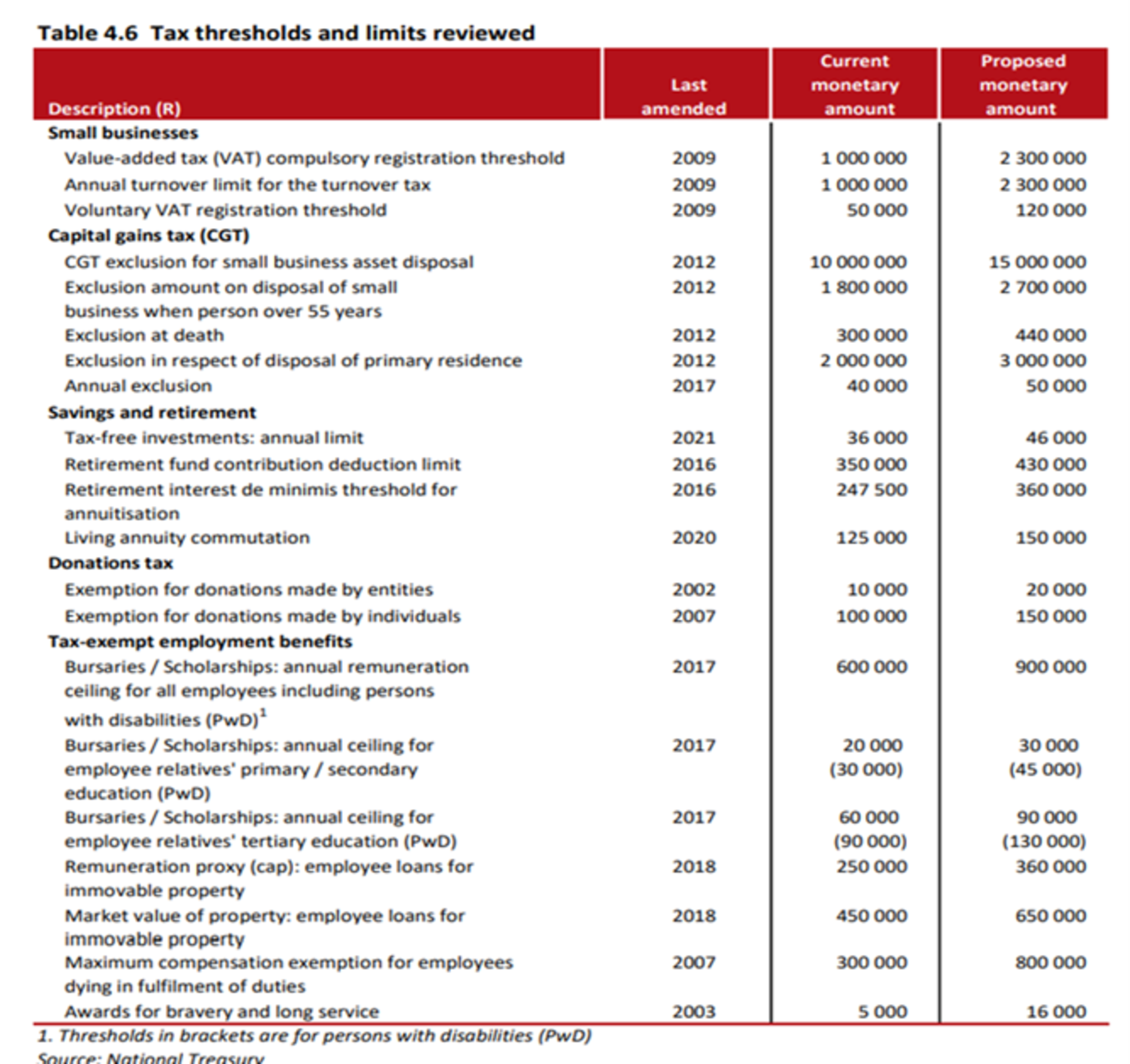

2.9 Threshold and limit adjustments To promote entrepreneurship, savings and a fairer tax regime for those receiving employment benefits, the thresholds in Table 4.6 will be adjusted for inflation. The VAT registration thresholds will be effective from 1 April 2026 while the other thresholds will be effective from 1 March 2026:

2.10 Excluding certain exempt entities that are companies from the definition of “provisional taxpayer” The definition of “provisional taxpayer” in the Fourth Schedule of the Income Tax Act excludes certain entities that are subject to partial taxation. The exclusion of these entities was mainly aimed at reducing their compliance burden, for example, the difficulty in determining how provisional tax should apply to amounts subject to exemption only up to a specified threshold. In terms of paragraph (b) of the definition of “provisional taxpayer”, any company is a provisional taxpayer. It is thus proposed that fully exempt entities and certain partially exempt entities, which are regarded as companies, should also be excluded from being classified as provisional taxpayers.

2.11 Reviewing penalty regime for underestimation of provisional tax To trigger the penalty for underestimating provisional tax, a taxpayer must first underestimate their taxable income outside acceptable tolerances. If the taxpayer submits an estimate that is within the acceptable tolerance but pays no provisional tax, the underestimation penalty cannot be imposed. The only penalty applicable in these instances is the lesser late payment penalty. It is proposed that, with effect from 25 February 2026, timely payment of the amount of the estimate be required before it may be relied on. There are existing rules to ensure that there is no duplication of the underestimation and the late payment penalties. Furthermore, the R1 million cap for relying on amounts based on historical assessments, rather than current estimates, will be increased to R1.8 million for years of assessment commencing on or after 1 March 2026.

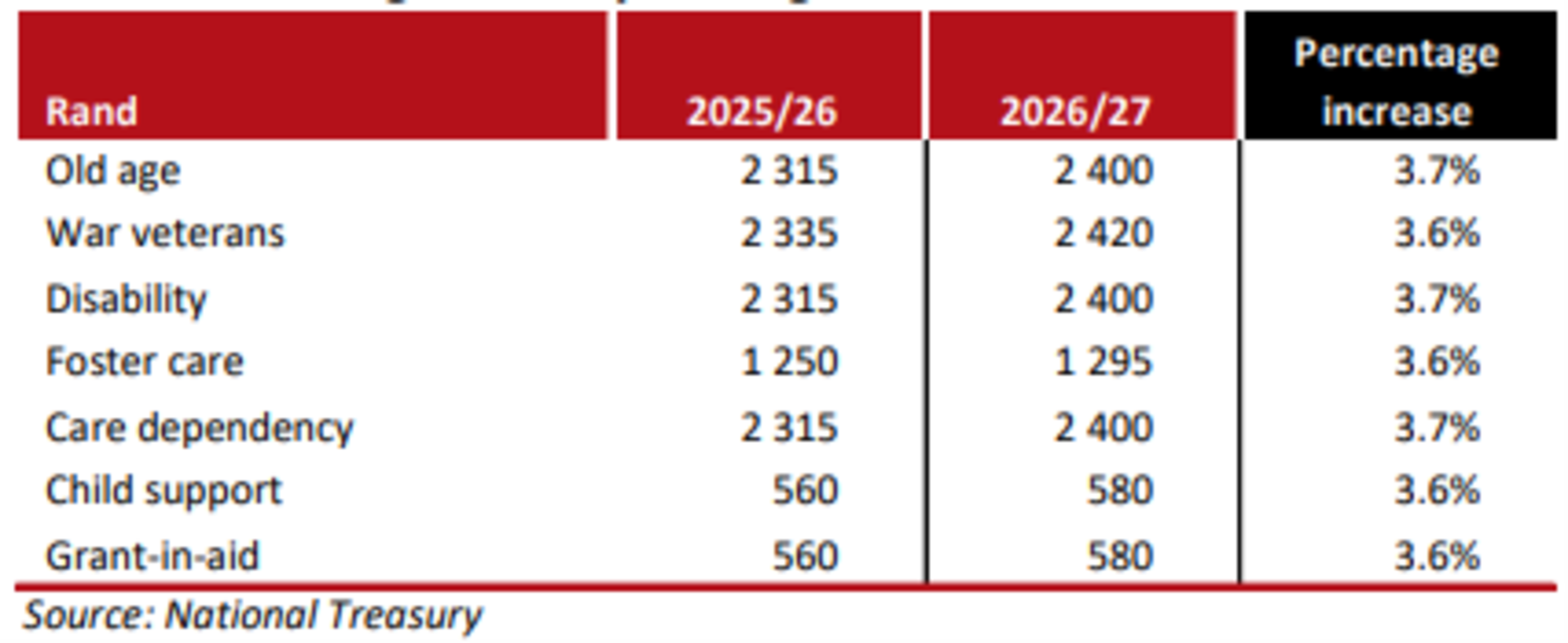

The old age grant, disability grant and care dependency grant will increase to R2 400 in April 2026, while the war veterans grant increases to R2 420. The foster care grant will increase to R1 295. The child support grant and grant-in-aid grant rise to R580. The social relief of distress grant is allocated an additional R36.4 billion to extend payments until 31 March 2027 at the current R370 per month per beneficiary.

The social grant increase is as per the table:

4.1 Retirement fund contribution deduction limits Currently, members contributing to a retirement fund may receive a tax deduction for contributions made to a retirement fund of up to 27.5% on the greater of remuneration or taxable income, but not more than R350 000 per annum. This means that a member may not deduct contributions for tax purposes of more than the annual limit of R350 000. This amount will be increased to R430 000 effective 1 March 2026.

4.2 Retirement interest de minimis (commutation) threshold for annuitisation Currently, at retirement, everything in the retirement component must be used to purchase an annuity – subject to the de minimis amounts which are calculated cumulatively across the entire retirement component and the non-vested portion of the vested component. The current de minimis is R247 500. This de minimis will be increased to R360 000 effective 1 March 2026.

4.3 Living annuity commutation The conditions for when a living annuity may be commuted is set out in the Income Tax Act. Paragraph (c) of the definition of living annuity in the Income Tax Act deals with commutation of a living annuity. It provides that the full remaining value of the living annuity may be paid in a lump sum when the value at any time becomes less than the amount prescribed by the Minister of Finance. The current prescribed amount of R125 000 will be increased to R150 000.

4.4 Determining the application of the de minimis (commutation) limit for multiple living annuities held with the same insurer or fund The Income Tax Act allows a living annuity to be commuted and paid as a lump sum when the value of the assets falls below the prescribed de minimis limit, currently set at R125 000 (which will be increased to R150 000 as of 1 March 2026). This limit is applied on a per-insurer or per-fund basis, depending on whether the living annuity is provided by the fund or purchased from an insurer, whereby the value of all living annuities held by an annuitant with the same insurer or fund is aggregated when applying the limit. However, differing interpretations of the law exist regarding whether this limit applies per policy or cumulatively per insurer or fund. Applying the limit on a per-policy basis could undermine retirement income security by enabling the early commutation of multiple small annuities and facilitating tax-driven restructuring of retirement assets. It is therefore proposed that the definition of “living annuity” in section 1 of the Income Tax Act be amended to explicitly provide that the prescribed de minimis limit must be determined cumulatively where an annuitant holds multiple living annuities with the same insurer or fund.

4.5 Unclaimed assets Government is implementing a reform to centralise the management and investment of over R88 billion in unclaimed financial assets, which include retirement benefits, bank accounts, investments and insurance payouts. This reform aims to ensure that the benefits of these assets accrue to the asset owners rather than to financial institutions, government or any other parties. The proposed framework provides for the transfer of these assets to a central manager to drive down costs and improve payouts with appropriate governance for investment, alongside the appointment of a central administrator responsible for administration, record-keeping and tracing. The reform will be rolled out in phases, starting with the retirement fund sector, given its established identification and monitoring systems. Over time, the framework will be extended to other categories of unclaimed financial assets. The centralisation of unclaimed financial assets seeks to address challenges associated with fragmented administration, inconsistent definitions and the erosion of value through fees. A unified system, supported by a central database and an administrator, is intended to strengthen tracing processes and enhance transparency. It is also expected to provide beneficiaries with a clearer and more streamlined claims process. A discussion note will be released shortly for public consultation.

4.6 Infrastructure investing The Minister indicated that infrastructure is attracting significant private sector investment. National Treasury and Development Bank of South Africa is currently setting up the Infrastructure Finance and Implementation Support Agency. The key focus areas are electricity transmission, transport, water, telecoms and visas. There are currently 63 public private partnerships/projects that are being managed.

5.1 Preparing for the 2026/27 FATF mutual evaluation South Africa exited the Financial Action Task Force (FATF) grey list in October 2025. Preparations have begun for the next round of assessment, from mid-2026 to October 2027. Regulatory and legislative measures to further bolster the financial system’s ability to combat financial crime will be brought to Parliament early in 2026. These include the General Laws (Anti-Money Laundering and Combating Terrorism Financing) Amendment Bill, which the National Treasury published for public comment in January 2026. The draft bill proposes amendments to the Financial Intelligence Centre Act (2001), the Financial Sector Regulation Act (2017), the Companies Act (2008) and the Nonprofit Organisations Act (1997) and seeks to address some technical deficiencies.

5.2 Implementation of an open finance framework Open finance is the framework that allows individuals and businesses to safely share their financial data with third-party providers, with their explicit consent, in order to access better, more competitive and more innovative financial products and services. It has the potential to drive down the cost of financial services for individuals and businesses. In 2025, the IFWG finalised a comprehensive cost-benefit analysis that set out concrete recommendations to guide the implementation of an open finance framework in South Africa. Over the next financial year, the IFWG will continue with work to develop an appropriate regulatory framework for open finance.

5.3 Regulating artificial intelligence in the financial sector The Financial Sector Conduct Authority (FSCA) and the Prudential Authority undertook a survey on the adoption of artificial intelligence (AI) in the South African financial sector. This study provided insights into the usage and adoption of AI in the sector. The FSCA, the Prudential Authority and the Reserve Bank are collaborating to develop a discussion paper, based on the survey, to be published in July 2026. The paper will set out recommendations for the safe and responsible adoption of AI in the South African financial sector, with a view to developing a formal joint regulatory instrument.

5.4 Exploring the impact of influencers on financial consumers’ decision-making The FSCA is conducting a market study to explore the impact of influencers on financial consumers’ decision-making processes. As social media gains prominence as a significant source of information, financial information and, in particular, the role of financial consumer influencers – so-called “finfluencers” – has become more pronounced. The market study will be published in 2026.

5.5 Advancing climate-risk resilience in the financial sector Government continues to work to strengthen responses to climate-related and broader sustainability risks through the development of regulatory and supervisory tools. The Prudential Authority and the FSCA are assessing banks’ and insurers’ climate-related governance, risk practices and disclosures. The intention is to evaluate the maturity of these industries regarding their responses to climate risks and closely monitor the links between climate-related financial risks and nature-related risks and biodiversity loss. In 2026, the National Treasury will publish a consultation paper on transition planning by financial institutions to provide a framework for the content and nature of strategic planning that these institutions should undertake to address climate-related risks. These plans should include climate-related governance, risk practices and disclosures.

5.6 Capital flows management framework The National Treasury will publish amendments to the Exchange Control Regulations under the Currency and Exchanges Act (1933). The amendments aim to include crypto assets in the capital flows management framework to complement regulation by the FSCA, which officially declared crypto assets (like Bitcoin and Ethereum) to be “financial products” under the Financial Advisory and Intermediary Services Act (2002) from October 2022. Similar regulatory action has been taken by the Financial Intelligence Centre, which in 2025 designated crypto asset service providers as accountable institutions subject to supervision, including reporting, registration and enforcement.

5.7 Payments Modernisation and Digital Finance Payments Ecosystem Modernisation Programme

The Reserve Bank is leading the most significant reform of the payments system in nearly three decades, aimed at:

Faster, cheaper and more inclusive payments

Reduced reliance on cash

Greater innovation and resilience

National Payments Utility

A National Payments Utility (NPU) is being established through the transition of PayInc (formerly BankservAfrica), now majority owned by the Reserve Bank.

The NPU will provide shared digital infrastructure for high value and retail payments.

6.1 Public Sector Early Retirement Programme Government has begun implementing its Early Retirement Programme to rejuvenate the public-sector workforce and manage compensation costs. Since the programme commenced in October 2025, 7 687 applications have been approved, while R3.7 billion of the available amount has been drawn down. The estimated net saving from this programme is R5.5 billion, of which R2.6 billion will be realised in 2026/27, R1.4 billion in 2027/28 and R1.5 billion in 2028/29.

6.2 Early Childhood Development grant The Early Childhood Development (ECD) grant will receive an additional R12.8 billion over the next three years, enabling services to reach 300,000 more children. The budget also maintains the per child, per-day subsidy of R24, introduced in 2025/26. In addition, allocations have been increased to ensure the National School Nutrition Programme keeps pace with food inflation, continuing to provide meals to over 9.9 million learners in nearly 20,000 schools.

6.3 Collective investment schemes Following public consultation after the publication of the discussion paper on collective investment scheme (CIS) taxation in 2024, the National Treasury will release a response document with revised proposals for further consultation. The draft recommendation in the response document proposes that all investment returns generated by regular CISs and retail investment hedge funds be taxed as capital. This is to encourage savings and to provide the industry with certainty about the tax treatment of these savings vehicles. CISs and retail investment hedge funds are open to the general public, are well regulated and have diversification and other requirements, providing an important avenue for savings. By contrast, qualified investment hedge funds are not open to the general public, have minimal investment criteria and only cater for those able to invest a minimum of R1 million. Government will propose excluding such qualified funds from the CIS tax regime. Alternative tax regime options for these funds will be proposed in the response document.

In terms of the Minister’s proposal, the compulsory VAT registration threshold for small business will increases from R1 million to R2.3 million.

Furthermore, the capital gains tax exemption for the sale of a small business for older persons are raised from R1.8 million to R2.7 million. This applies to small businesses worth R15 million instead of the R10 million previously. It will enable small business owners to receive more tax relief when they sell their businesses.

Compiled by Carien Veenstra, Tholoana Makhu, Mumtaz Dawood, Sam Masetle, Wisdom Chauke

The budget proposals in this document by the Minister of Finance, are subject to ratification by Parliament. The information herein incorporates commentary from the budget speech, but the legislation finally enacted may differ. All information herein is believed to be correct at the time of publication, 25 February 2026. While we have taken utmost care in compiling this document, we accept no responsibility for any inaccuracies, errors or omissions.

This document is not intended to give advice, consequently the contents hereof should not be used as a basis for action without seeking your own professional advice. Tax rate changes proposed in the budget speech only becomes effective once legislation is enacted by Parliament. No part of this work may be altered or reproduced without the consent of SLS Legal Services.